|

|

Post by celo on Dec 6, 2022 16:51:34 GMT -5

Well..getting revenue estimates is one thing, EPS is a whole different animal. It would be hard to estimate how much mannkind has been increasing expenses for the amount of runtime to manufacture all the Tyvaso.

Edit: Cost of goods sold was 33 million for 1Q, 39 million for 2Q, 42 million for Q3. How about 48 million for Q4

Other expenses were ~5 million for Q3. Probably the same for Q4

So about break even for the quarter.

My revenue estimate may be on the high end, due to it coming off of symphony data. However, they do have 32 million of deferred revenue.

|

|

|

|

Post by prcgorman2 on Dec 6, 2022 16:59:52 GMT -5

I eagerly await a good EPS estimate. I think it will be positive EPS if we hit those numbers, but I assume we will also need a very good P/E for it to move the share price very much. I've assumed between $6 and $8 in 2023 which makes me no better than the lousy analysts. I think to see a crazy good P/E we're going to need a catalyst.

|

|

|

|

Post by peppy on Dec 6, 2022 17:00:19 GMT -5

Well..getting revenue estimates is one thing, EPS is a whole different animal. It would be hard to estimate how much mannkind has been increasing expenses for the amount of runtime to manufacture all the Tyvaso. Cost of goods sold was 42 million for Q3. How about 48 million for Q4 Other expenses were ~5 million. Probably the same for Q4 So about break even for the quarter.My revenue estimate may be on the high end, due to it coming off of symphony data. However, they do have 32 million of deferred revenue. Hence the measured move $12. That is my story and I am sticking to it. If it fails or starts to look like the target will fail, I'll scream out. |

|

|

|

Post by celo on Dec 7, 2022 13:06:39 GMT -5

4q 2022 will really be a bellwether for revenue going forward for Tyvaso DPI. At the end of this year, United has said they want 6k patients on Tyvaso.

From the 3Q report, Tyvaso and Tyvaso DPI are splitting those patients evenly. For ease and simplification, half or 3k patients using Tyvaso DPI by end of 2022. Probably that ratio will swing more in favor of DPI going forward.

From the November 2022 United report, they believe they will have 25k patients by the end of 2025. At that point in time, DPI should dominate with 60% of the patient mix. Probably be higher percentage, but we will say 60%.

That is a growth of 3k patients now, to 15k patients by the end of 2025. That represents a 5x growth in revenue in 3 years.

The 4Q will allow us to see DPI revenue potential because it will be the first qtr of stable week to week usage.

Therefore, projecting 4Q tyvaso revenue for Mannkind at 40 million (manufacturing and royalty payments) for 4Q 2022 gives the potential of 200 million revenue for 4Q25 or almost 800 million in annual revenue.

Using an 8 to 10x revenue multiple for market cap which is conservative as this would be a growth stock, allows for an 10 to 12 billion market cap. Or a price of 35-40 by 2025. Mannkind does have dilution due to the debt which would knock the price down a bit.

There should be other revenue possibilities knocking on the door after the multiple quarters success of Tyvaso DPI. Those should bear out at the end of 2023 as pharm companies see the continued uptake and use of DPI. Those factors into the price are hard to ascertain and may be large.

|

|

|

|

Post by sportsrancho on Dec 7, 2022 13:20:22 GMT -5

I love this post don’t get me wrong but right now growth company are valued at four times, hopefully over the next few years that will change. I remember 15times being the norm.

|

|

|

|

Post by peppy on Dec 7, 2022 14:14:20 GMT -5

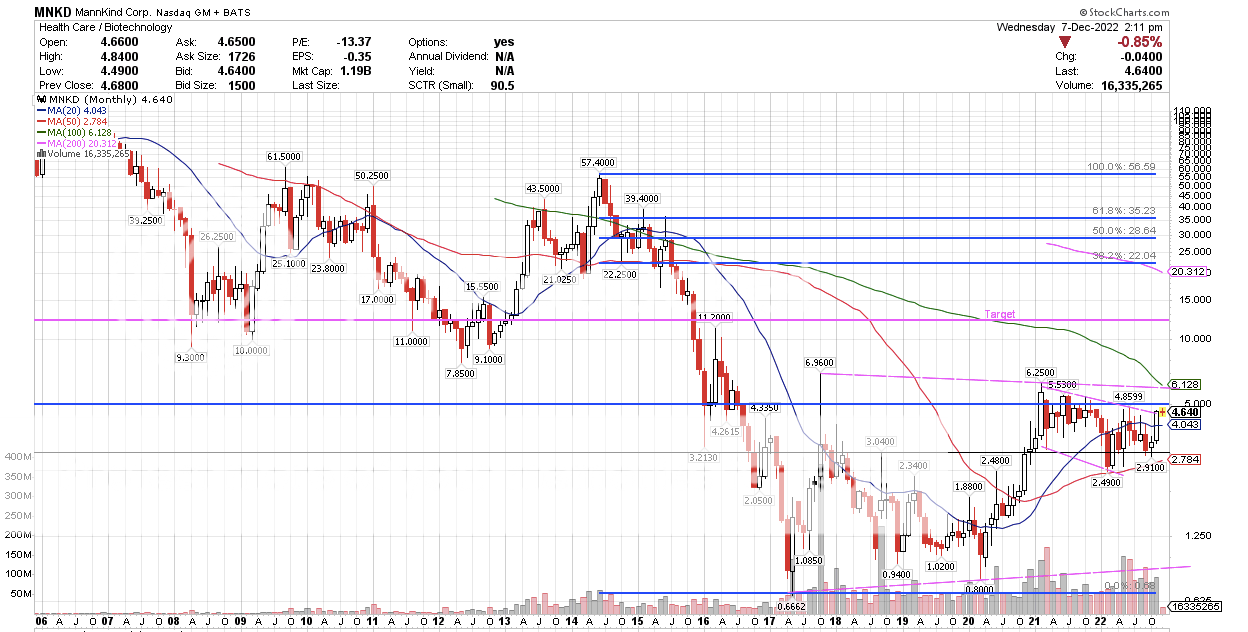

4q 2022 will really be a bellwether for revenue going forward for Tyvaso DPI. At the end of this year, United has said they want 6k patients on Tyvaso. From the 3Q report, Tyvaso and Tyvaso DPI are splitting those patients evenly. For ease and simplification, half or 3k patients using Tyvaso DPI by end of 2022. Probably that ratio will swing more in favor of DPI going forward. From the November 2022 United report, they believe they will have 25k patients by the end of 2025. At that point in time, DPI should dominate with 60% of the patient mix. Probably be higher percentage, but we will say 60%. That is a growth of 3k patients now, to 15k patients by the end of 2025. That represents a 5x growth in revenue in 3 years. The 4Q will allow us to see DPI revenue potential because it will be the first qtr of stable week to week usage. Therefore, projecting 4Q tyvaso revenue for Mannkind at 40 million (manufacturing and royalty payments) for 4Q 2022 gives the potential of 200 million revenue for 4Q25 or almost 800 million in annual revenue. Using an 8 to 10x revenue multiple for market cap which is conservative as this would be a growth stock, allows for an 10 to 12 billion market cap. Or a price of 35-40 by 2025. Mannkind does have dilution due to the debt which would knock the price down a bit. There should be other revenue possibilities knocking on the door after the multiple quarters success of Tyvaso DPI. Those should bear out at the end of 2023 as pharm companies see the continued uptake and use of DPI. Those factors into the price are hard to ascertain and may be large. every 4 dollar share price gain is a billion dollar market cap. 4.645. +0.075. (+1.6411%) Market Cap 1.221B projecting 4Q tyvaso revenue for Mannkind at 40 million (manufacturing and royalty payments) for 4Q 2022 gives the potential of 200 million revenue for 4Q25 or almost 800 million in annual revenue. Using an 8 to 10x revenue multiple for market cap which is conservative as this would be a growth stock, allows for an 10 to 12 billion market cap. Or a price of 35-40 by 2025. First target a 3 billion dollar market cap. (The way I am) doable. Let's see some monthly price impulse here. Anybody see the DRAGON?, (fire breathing dragon?) geomean,   |

|

|

|

Post by Thundersnow on Dec 7, 2022 14:34:54 GMT -5

4q 2022 will really be a bellwether for revenue going forward for Tyvaso DPI. At the end of this year, United has said they want 6k patients on Tyvaso. From the 3Q report, Tyvaso and Tyvaso DPI are splitting those patients evenly. For ease and simplification, half or 3k patients using Tyvaso DPI by end of 2022. Probably that ratio will swing more in favor of DPI going forward. From the November 2022 United report, they believe they will have 25k patients by the end of 2025. At that point in time, DPI should dominate with 60% of the patient mix. Probably be higher percentage, but we will say 60%. That is a growth of 3k patients now, to 15k patients by the end of 2025. That represents a 5x growth in revenue in 3 years. The 4Q will allow us to see DPI revenue potential because it will be the first qtr of stable week to week usage. Therefore, projecting 4Q tyvaso revenue for Mannkind at 40 million (manufacturing and royalty payments) for 4Q 2022 gives the potential of 200 million revenue for 4Q25 or almost 800 million in annual revenue. Using an 8 to 10x revenue multiple for market cap which is conservative as this would be a growth stock, allows for an 10 to 12 billion market cap. Or a price of 35-40 by 2025. Mannkind does have dilution due to the debt which would knock the price down a bit. There should be other revenue possibilities knocking on the door after the multiple quarters success of Tyvaso DPI. Those should bear out at the end of 2023 as pharm companies see the continued uptake and use of DPI. Those factors into the price are hard to ascertain and may be large. every 4 dollar share price gain is a billion dollar market cap. 4.645. +0.075. (+1.6411%) Market Cap 1.221B projecting 4Q tyvaso revenue for Mannkind at 40 million (manufacturing and royalty payments) for 4Q 2022 gives the potential of 200 million revenue for 4Q25 or almost 800 million in annual revenue. Using an 8 to 10x revenue multiple for market cap which is conservative as this would be a growth stock, allows for an 10 to 12 billion market cap. Or a price of 35-40 by 2025. First target a 3 billion dollar market cap. (The way I am) doable. Let's see some monthly price impulse here. Anybody see the DRAGON?, (fire breathing dragon?) geomean , Actually I do. I see the head at $57.40 (2014) and the feet at $1.085 & $1.02 with a Hammertoe at $.94 (My joke) and the "FIRE" from 2006 - 2014.....Holy cow......The Run could be enormous if it plays out over time. |

|

|

|

Post by Thundersnow on Dec 7, 2022 15:18:36 GMT -5

|

|

|

|

Post by celo on Dec 7, 2022 21:01:47 GMT -5

I love this post don’t get me wrong but right now growth company are valued at four times, hopefully over the next few years that will change. I remember 15times being the norm. The difference with Mannkind's growth and most growth companies is profitability is visible on the horizon. Mannkind has already shown that with Afrezza and it should be pretty easy with Tyvaso DPI. Most growth companies show large year over year revenue but massive losses to get there and have not begun functioning profitably. Mannkind is currently at a 12x cap/revenue ratio. Unfortunately or fortunately, you can look at it either way, Mannkind is a mature/immature company. Immature in it's other possible revenue streams. Mature when it comes to production of Afrezza, growth has slowed and now is profitable. If Mannkind can show the same profitability on Tyvaso DPI, which I believe is pretty easy with the construct of the contract with United and the length of time tweaking their production line, then the 12x will be warranted, especially by 2025. IMO the royalty percent is somewhere around 12 to 13 which allows easier calculations. |

|

|

|

Post by dh4mizzou on Dec 8, 2022 7:19:13 GMT -5

|

|

Deleted

Deleted Member

Posts: 0

|

Post by Deleted on Dec 8, 2022 9:00:50 GMT -5

Puff, Puff...Pass

|

|

|

|

Post by prcgorman2 on Dec 8, 2022 12:40:53 GMT -5

I hear the train a-comin, coming round the bend, and I ain't seen the sunshine, since I don't know when. I'm stuck in MNKD prison and time keeps DRAGON on...

There needs to be more than the current revenues from V-Go, Afrezza, and manufacturing revenue and royalties from Tyvaso DPI if we want the dragon to look more like Smaug and less like the friendly female dragon from Shrek.

The future is bright, but much brighter still if...

|

|

Deleted

Deleted Member

Posts: 0

|

Post by Deleted on Dec 8, 2022 16:52:03 GMT -5

Made me think about the song...Puff the Magic Dragon... |

|

|

|

Post by prcgorman2 on Dec 9, 2022 0:46:42 GMT -5

Made me think about the song...Puff the Magic Dragon... I thought you had two meanings; Puff the Magic Dragon, and the kind of puffing and passing that happens with a joint (i.e., a marijuana cigarette). Your reference to Puff the Magic Dragon was what made me think of the stanza from Johnny Cash’s famous Folsom Prison Blues. |

|

Deleted

Deleted Member

Posts: 0

|

Post by Deleted on Dec 9, 2022 8:59:29 GMT -5

Made me think about the song...Puff the Magic Dragon... I thought you had two meanings; Puff the Magic Dragon, and the kind of puffing and passing that happens with a joint (i.e., a marijuana cigarette). Your reference to Puff the Magic Dragon was what made me think of the stanza from Johnny Cash’s famous Folsom Prison Blues. It has always been said the song was about smoking weed. |

|