|

|

Post by mbseeking on Apr 14, 2016 0:41:37 GMT -5

old saw, was it just me... or was the the timing of the bankruptcy piece odd. I mean its old news, right? just seem to slip out at a time to nix a little run up ..

|

|

|

|

Post by babaoriley on Apr 14, 2016 1:25:26 GMT -5

The Mann Group owns about 45% of the common stock. That gets wiped out. If they own preferred stock that normally does not. The common stock holder is toasted. I would guess they would sell the company before having to have a bankruptcy situation. I sure hope so as I have too many underwater shares.

I would hope that the board would put the company up for sale if they haven't yet? I would bet there would be a bidding war for the company. based on the length of how long one has held the stock most longs have hopefully averaged down their share cost. I know that mine is not about $5.50 per share. That is not great but I would be happy to get my invested cost out of the shares at this time. So if the company was sold in a bidding war maybe they could get a low ball offer to start the bidding at about $5.00 per share and possibly end up at $12 to $25.00 per share. Maybe not the great win that we all had wanted back in 2014 but then again most folks would be whole and out of the company.

Personally I don't see a bankruptcy in the future for MannKind. Too much value to see it not get purchased by a Smart Nimble Pharma who can take Afrezza and Technosphere to the market. Afrezza is what the diabetic market needs and will eventually be the gold standard for treatment for T1, T2, and yes Pre-diabetes. Wow, kc, just wow! The great win I thought about in 2014 was $25/share! Maybe more if we were real lucky with Technosphere. But now, the great win I would think about would be $4 or so per share. I would consider that a "great win" under these most uncertain circumstances. |

|

|

|

Post by kc on Apr 14, 2016 5:45:52 GMT -5

The reality is that most big pharma know that's the value of this company is a lot more in a starting bid of $4. And we have a good FDA-approved product that is worth at least $12. Let the bidding begin.

|

|

|

|

Post by patten1962 on Apr 14, 2016 6:02:03 GMT -5

The reality is that most big pharma know that's the value of this company is a lot more in a starting bid of $4. And we have a good FDA-approved product that is worth at least $12. Let the bidding begin. Just don't want a buyout. Think this could be a stock that trades 20x earnings. Just think if Afrezza picks up with Mike in charge! Could we possibly be a $20 to 30 stock by November? You guys tell me. |

|

|

|

Post by sportsrancho on Apr 14, 2016 6:11:20 GMT -5

The reality is that most big pharma know that's the value of this company is a lot more in a starting bid of $4. And we have a good FDA-approved product that is worth at least $12. Let the bidding begin. Just don't want a buyout. Think this could be a stock that trades 20x earnings. Just think if Afrezza picks up with Mike in charge! Could we possibly be a $20 to 30 stock by November? You guys tell me. We are 18 months behind so let's give it till the middle of 2018:-) |

|

|

|

Post by patten1962 on Apr 14, 2016 6:17:45 GMT -5

Just don't want a buyout. Think this could be a stock that trades 20x earnings. Just think if Afrezza picks up with Mike in charge! Could we possibly be a $20 to 30 stock by November? You guys tell me. We are 18 months behind so let's give it till the middle of 2018:-) Let's just say 3rd Q sales are 4x greater then now, what would happen? I don't want to put a $ figure on that because I have no idea the cost of advertising! I am talking just Afrezza sales. Thanks.  |

|

|

|

Post by sportsrancho on Apr 14, 2016 6:25:03 GMT -5

We are 18 months behind so let's give it till the middle of 2018:-) Let's just say 3rd Q sales are 4x greater then now, what would happen? I don't want to put a $ figure on that because I have no idea the cost of advertising! I am talking just Afrezza sales. Thanks. Just guessing, first we need money to get us a few years down the road. With scripts at 2,000 per week. Gets us to 12pps? |

|

|

|

Post by patten1962 on Apr 14, 2016 6:37:50 GMT -5

Let's just say 3rd Q sales are 4x greater then now, what would happen? I don't want to put a $ figure on that because I have no idea the cost of advertising! I am talking just Afrezza sales. Thanks. Just guessing, first we need money to get us a few years down the road. With scripts at 2,000 per week. Gets us to 12pps? I am good with that! |

|

|

|

Post by mnholdem on Apr 14, 2016 7:19:43 GMT -5

Let's just say 3rd Q sales are 4x greater then now, what would happen? I don't want to put a $ figure on that because I have no idea the cost of advertising! I am talking just Afrezza sales. Thanks. Just guessing, first we need money to get us a few years down the road. With scripts at 2,000 per week. Gets us to 12pps?

Mannkind stock, hopes rise again

By Dirk Perrefort

Published 3:27 pm, Wednesday, April 13, 2016

Some have speculated that the company could be nearing bankruptcy as it only has enough cash on hand to operate through the second half of the year. However, chief executive officer Matt Pfeffer has said the company is looking at a variety of options, including potential licensing deals, that could provide additional cash for future operations.

Source: www.newstimes.com/business/article/Mannkind-stock-hopes-rise-again-7246467.php

---

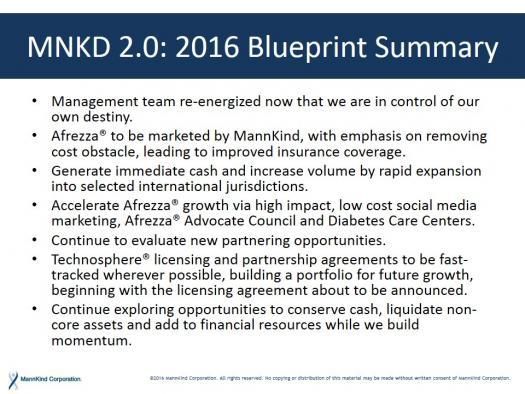

MannKind 2.0

Conspicuous by its absence in recent press releases is bullet point #3 related to sales of Afrezza outside the U.S. Shareholders were told that two regional drug companies called MannKind within 24 hours of the announcement that the MannKind/Sanofi License & Collaboration Agreement was being terminated.

Since Matt made those remarks about parties showing interest in Afrezza, he has said nothing further. Why? There are two possible reasons:

- The inquiries and subsequent discussions did not result in any further discussions, or;

- Commencing April 5, with the return of global marketing rights for Afrezza, MannKind & its potential partner(s) are currently negotiating Agreements under a Non-Disclosure Agreement.

You'll notice the purpose of this MannKind 2.0 objective is to "generate immediate cash and increase volume by rapid expansion". CEO Pfeffer needs to address the cash burn and this is the best way to accomplish it. Large initial orders for stocking pharmacies followed by regional sales will result in MannKind firing up their 3 lines, which will result in lowering of COGS to manufacture Afrezza, resulting in even greater profits.

Matt once told me that further plant expansion would be linked to expansion into international markets, so it's likely that an upfront payment would be substantial enough for MannKind to order and install additional lines for producing Afrezza.

---

In addition to the Receptor Life Sciences licensing deal, with its potential $102M + commercial royalties, there is also the possibility of another drug partnership for Epinephrine(TS), which will soon complete the Technology Assessment Phase and be ready for an Investigational New Drug filing with the FDA. You'll notice the black bar on the graph below entitled, "Business Opportunities"? What this timeline is showing us is that once a Go/NoGo decision has been reached, a partner will be sought for further development and marketing of Epinephine(TS) and an upfront payment & royalties agreement will likely accompany the deal.

MannKind retains the option to develop this drug on its own, and with shareholders authorizing an additional 150 million shares of common stock, management would have the funds to do it. This is the drug that requires no FDA trial, as explained by Dr. Urbanski at the 13-Jan-2016 JPOM Conference:

"The last slide, the last one of our clinical development candidates is Epinephrine for Anaphylaxis. I think the one point I want to raise here is this can be an incredibly short timeline. No real clinical studies would be required. Obviously you cannot do a clinical study in the Anaphylactic setting. So that would be e-study and some human factor studies would probably suffice. So we're looking at this opportunity as again one of our priority ones." - Dr. Raymond Urbanski, CMO MannKind Corporation

I think it's likely that MannKind will announce a partnership for further development of Epinephrine(TS) sometime during the 2nd or 3rd Quarter.

---

The point is, things are hardly as financially bleak as some would have us believe. The authorization of additional common stock is meant to both insure continued operations and development, as well as to provide us with better leverage in negotiations with pharmaceutical company negotiations.

|

|

|

|

Post by sportsrancho on Apr 14, 2016 8:37:26 GMT -5

Agree! Right now our name is mud on WS. Once we getting rolling we will be re-branded as a growth company. Then we shoot to the moon:-)))

|

|

|

|

Post by kc on Apr 14, 2016 11:07:30 GMT -5

I have said all along we are better if they sell the company. Who know if that is on the table but I would guess that they would sell it before having file a chapter 11 case. But what do I know as a dumb investor.

|

|

|

|

Post by babaoriley on Apr 14, 2016 12:38:58 GMT -5

kc, if their choice is between BK and selling the company, don't expect buy out numbers like those being thrown around cavalierly on this thread.

Has everyone taken leave of their senses again?

|

|

|

|

Post by kc on Apr 14, 2016 19:11:29 GMT -5

kc, if their choice is between BK and selling the company, don't expect buy out numbers like those being thrown around cavalierly on this thread. Has everyone taken leave of their senses again? Baba My figure was just a starting point. I believe that all together the company today is worth $20-$25 per-share. I see a bidding war situation. But as I stated I'm just a dumb businessman Who bought shares of this company and kept buying shares. So perhaps I am not so bright . |

|

|

|

Post by sportsrancho on Apr 14, 2016 19:23:48 GMT -5

kc, if their choice is between BK and selling the company, don't expect buy out numbers like those being thrown around cavalierly on this thread. Has everyone taken leave of their senses again? Baba My figure was just a starting point. I believe that all together the company today is worth $20-$25 per-share. I see a bidding war situation. But as I stated I'm just a dumb businessman Who bought shares of this company and kept buying shares. So perhaps I am not so bright . I believe BP knows this and are just hoping we go under. When this turns around and I think the turning point is soon, you'll be the smartest man on the ship kc:-) |

|