|

|

Post by promann on Feb 14, 2017 11:39:56 GMT -5

True, but I believe those are for continued listing under normal circumstances. Folks are getting CONTINUED listing standards mixed up with INITIAL listing standards. They are different. The delisting notice says in plain language that MNKD must meet initial listing standards. A company in good standing on the Nasdaq would fall under these CONTINUED listing requirements. MNKD currently faces a delisting notice from Nasdaq, and per the delisting notice MNKD will need to meet INITIAL listing standards in order to qualify for additional time to remedy the share price deficiency. The delisting notice indicates that MNKD will have to meet ALL initial listing requirements, which require a minimum $5 million in shareholder equity. It does not meet this requirement. It is ridiculous that you have to keep explaining this. We've been over this SO many times on this forum. I know I also explained it several times, until I got fed up. Some of my prior posts are in here: mnkd.proboards.com/thread/6235/nasdaq-share-price-compliance-notice?page=2In particular, for the doubters, note that Mannkind's OWN 8-K states they must ALSO satisfy "all other standards for INITIAL listing of its common stock on the NASDAQ Capital Market". That IS what Mannkind's own 8-K says. Of course, the NASDAQ site says the same thing (see second link below). investors.mannkindcorp.com/secfiling.cfm?filingID=1193125-16-716458&CIK=899460 Yes, the INITIAL listing requirements must be satisfied to avoid delisting. Those initial listing requirements may be found here: listingcenter.nasdaq.com/assets/initialguide.pdf It really is ridiculous how many times do we have to explain that Mannkind will be approved for the 2nd 180 day extension.,. geeze why cant you read it right! |

|

|

|

Post by 2011mnkdguy on Feb 14, 2017 11:44:07 GMT -5

THE DELISTING PROCESS 1. Deficiency Notice: If a company listed on the NCM fails to meet the minimum bid price requirement for a period of thirty consecutive trading days, it can expect to receive a deficiency notice from NASDAQ. The deficiency notice will identify the listing deficiency and will provide that the company has a period of 180 calendar days during which to regain compliance with the continued listing requirements. In order to regain compliance (if the deficiency is based on the failure to maintain the minimum bid price), the company’s closing bid price must be at or above $1.00 for a minimum of ten consecutive trading days during such period. Within four business days of the receipt of the deficiency notice, a company must publicly disclose the receipt of the deficiency notice by filing an 8-K with the SEC. The 8-K must disclose the date the deficiency notice was received, describe the listing requirement the company has failed to satisfy and detail any action it plans to take in response to such deficiency notice. NASDAQ maintains a list of non-compliant companies which is updated daily and posted at www.nasdaq.com. 2. Additional Compliance Period for NCM Listed Companies: If a company listed on the NCM is unable to regain compliance with the $1.00 minimum bid price requirement within the initial 180 day period, it will receive a second 180 day grace period provided the company (a) has at least $1 million in market value of shares held by non-affiliates and satisfies all of the other listing requirements for initial listing on the NCM (except the bid price requirement) and (b) notifies NASDAQ of its intent to cure the listing deficiency. If it does not appear to NASDAQ that it is possible for the company to cure the deficiency, this second grace period will not be granted. 3. Delisting Letter: If a company is unable to regain compliance within the grace period (including the additional grace period, if available), NASDAQ will issue a delisting letter. Within four business days of the receipt of the delisting letter, the company must publicly announce the receipt of the letter by filing an 8-K with the SEC. 4. Hearing: Upon receipt of a delisting letter the company will have seven days to submit a written request for a hearing before the NASDAQ Listing Qualifications Panel. The timely submission of this request will stay the delisting process pending the decision of the panel. At a hearing the company will be required to present a plan to regain compliance with the continued listing standards. The plan of compliance should describe the manner in which the company will regain and maintain compliance with the NASDAQ continued listing standards. NASDAQ has stated that the plan should include the implementation of a reverse stock split in the near term – no later than 180 days after receipt of the delisting letter. In determining whether to provide the company with the opportunity to implement its plan of compliance, the panel may consider other factors such as the company’s fundamental financial strengths and weaknesses, the overall market, the company’s historical bid price and impending corporate actions. Fees for a hearing range up to $5,000. 5. Failure to Request a Hearing: If the company does not request a hearing, upon the expiration of the seven day period NASDAQ will suspend trading of the security and proceed with the delisting. 6. Additional Appeals: If the panel determines to proceed with the delisting, the company will have fifteen days to appeal the panel’s decision to the NASDAQ Listing and Hearing Review Council. It may also appeal any NASDAQ decision in federal court. These actions will not stay the delisting process. |

|

|

|

Post by mnkdfann on Feb 14, 2017 11:44:58 GMT -5

It really is ridiculous how many times do we have to explain that Mannkind will be approved for the 2nd 180 day extension.,. geeze why cant you read it right! I'm talking about what the regulations state, not what will or will not happen. NASDAQ is free to do whatever it wants. |

|

|

|

Post by matt on Feb 14, 2017 11:46:39 GMT -5

You speak a half-truth. NASDAQ does require that "all the criteria must be met..." but you failed to mention "under at least one of the three standards below". Obviously you've selected the Equity Standard to make your argument, but MannKind may qualify using the Market Value Standard or Total Assets/Total Revenue Standard, neither of which has a Stockholders' Equity minimum requirement. You posted the wrong chart. There are three markets within NASDAQ: Global Select, Global Market, and Capital Market. Each of the three has initial listing requirements and each has continued listing requirements; you cannot mix and match the categories. Since Mannkind is a Capital Market company, it must meet the continued listing standards for the Capital Market. The chart you posted is for Global Select companies, but since Mannkind was never a Global Select company they cannot use those continued listing standards. Silentknight is correct that Capital Market companies must be compliant with all continued listing standards (except the $1 bid price) in order to qualify for the second 180 compliance period. The three Capital Market initial listing alternatives require either $4 million or $5 million in shareholder equity (per the most recent SEC filed financial statements). Forgiveness of the Sanofi debt and the settlement payment helps with that of course, but Mannkind is still close to $200 million below the minimum initial listing standard, and getting a special exemption when the company is that far out of compliance is not likely to happen. |

|

Deleted

Deleted Member

Posts: 0

|

Post by Deleted on Feb 14, 2017 12:06:18 GMT -5

In a worse case scenario: MannKind is not granted an extension; Board authorizes a reverse split; MannKind dilutes. If that is required to give MannKind time to make Afrezza the blockbuster it has the potential to be, so be it.

|

|

|

|

Post by silentknight on Feb 14, 2017 12:29:05 GMT -5

It is ridiculous that you have to keep explaining this. We've been over this SO many times on this forum. I know I also explained it several times, until I got fed up. Some of my prior posts are in here: mnkd.proboards.com/thread/6235/nasdaq-share-price-compliance-notice?page=2In particular, for the doubters, note that Mannkind's OWN 8-K states they must ALSO satisfy "all other standards for INITIAL listing of its common stock on the NASDAQ Capital Market". That IS what Mannkind's own 8-K says. Of course, the NASDAQ site says the same thing (see second link below). investors.mannkindcorp.com/secfiling.cfm?filingID=1193125-16-716458&CIK=899460 Yes, the INITIAL listing requirements must be satisfied to avoid delisting. Those initial listing requirements may be found here: listingcenter.nasdaq.com/assets/initialguide.pdf It really is ridiculous how many times do we have to explain that Mannkind will be approved for the 2nd 180 day extension.,. geeze why cant you read it right! Please tell us why you believe they will be approved when the rules run contrary to that thought. I am legitimately interested in knowing why. MNKD could receive it but to state it with such assurance is eerily reminiscent of your prediction for the conference call and disbelief with the R/S, which was completely incorrect. |

|

|

|

Post by gamblerjag on Feb 14, 2017 12:29:19 GMT -5

let me make this easy.. I was invested in this company called Ivanhoe energy.. This company had no assets, no money and no future.. It received an 180 ext. I'd be shocked that MNKD doesn't. I'm not saying that MNKD will get the ext since no one knows.. but I'm 95% sure they will..

|

|

|

|

Post by mnholdem on Feb 14, 2017 12:30:40 GMT -5

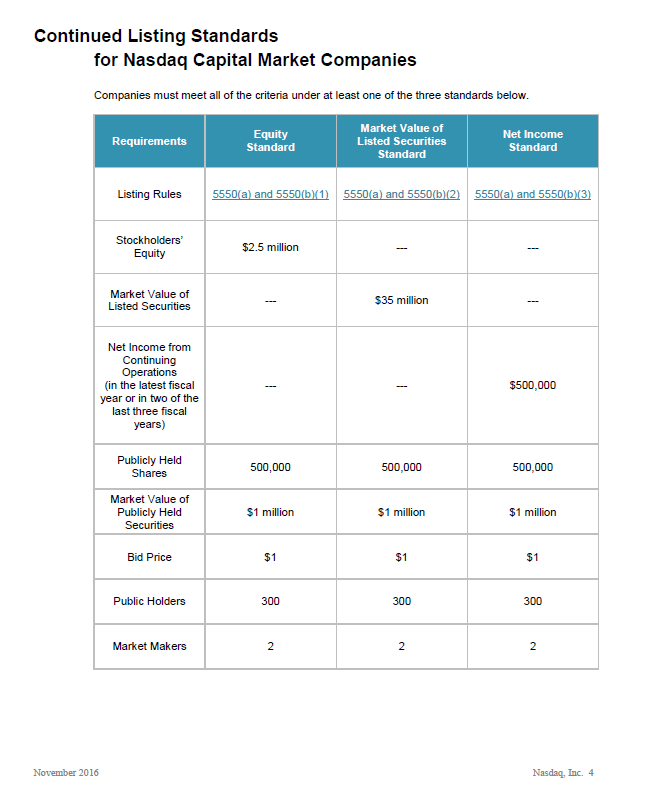

You speak a half-truth. NASDAQ does require that "all the criteria must be met..." but you failed to mention "under at least one of the three standards below". Obviously you've selected the Equity Standard to make your argument, but MannKind may qualify using the Market Value Standard or Total Assets/Total Revenue Standard, neither of which has a Stockholders' Equity minimum requirement. You posted the wrong chart. There are three markets within NASDAQ: Global Select, Global Market, and Capital Market. Each of the three has initial listing requirements and each has continued listing requirements; you cannot mix and match the categories. Since Mannkind is a Capital Market company, it must meet the continued listing standards for the Capital Market. The chart you posted is for Global Select companies, but since Mannkind was never a Global Select company they cannot use those continued listing standards. Silentknight is correct that Capital Market companies must be compliant with all continued listing standards (except the $1 bid price) in order to qualify for the second 180 compliance period. The three Capital Market initial listing alternatives require either $4 million or $5 million in shareholder equity (per the most recent SEC filed financial statements). Forgiveness of the Sanofi debt and the settlement payment helps with that of course, but Mannkind is still close to $200 million below the minimum initial listing standard, and getting a special exemption when the company is that far out of compliance is not likely to happen. Here is the Capital Market table.

I thought that SilentKnight stated that the Continued Listing Standards don't apply, that MannKind must meet the "Initial Listing Standards", but whatever. To have to meet all three standards, it seems to me, would eliminate half the biotech companies listed on NASDAQ who have never generated a penny of revenue and who never posted a shareholder equity of $2.5 million. I was focusing on the different standards and the comment that the company must meet at least one of those standards. I'll simply contact NASDAQ and post their reply like I did once before on a different topic. Thanks for directing me to the correct table.

Incidentally, the SEC filing stated that MannKind is listed on the Global Markets. That's why I posted that chart. From the Sept-2016 SEC filing about the delisting notice:

"Under Nasdaq Listing Rule 5810(c)(3)(A), if during the 180 calendar day period following the date of the Nasdaq Letter (the “Compliance Period”), the closing bid price of the Company’s common stock is at or above $1.00 for a minimum of 10 consecutive business days, the Company will regain compliance with the Minimum Bid Price Requirement and its common stock will continue to be eligible for listing on the Nasdaq Global Market absent noncompliance with any other requirement for continued listing."

|

|

|

|

Post by silentknight on Feb 14, 2017 12:55:19 GMT -5

For full transparency, I've posted the Initial Listing Standards for the Nasdaq Capital Market.

5505. Initial Listing of Primary Equity Securities

A Company applying to list its Primary Equity Security on the Capital Market must meet all of the requirements set forth in Rule 5505(a) and at least one of the Standards in Rule 5505(b).

(a) Initial Listing Requirements for Primary Equity Securities:

(1) (A) Minimum bid price of $4 per share; or

(B) Minimum closing price of $3 per share, if the Company meets the requirements of the Equity or Net Income Standards under Rules 5505(b)(1) or (b)(3), or of $2 per share, if the Company meets the requirements of the Market Value of Listed Securities Standard under Rule 5505(b)(2), provided that in either case the Company must also demonstrate that it has net tangible assets (i.e., total assets less intangible assets and liabilities) in excess of $2 million, if the issuer has been in continuous operation for at least three years; or net tangible assets in excess of $5 million, if the issuer has been in continuous operation for less than three years; or average revenue of at least $6 million for the last three years. A security must meet the applicable closing price requirement for at least five consecutive business days prior to approval.

For purposes of this paragraph (B), net tangible assets or average revenues must be demonstrated on the Company's most recently filed audited financial statements filed with, and satisfying the requirements of, the Commission or Other Regulatory Authority, and which are dated less than 15 months prior to the date of listing.

(2) At least 1,000,000 Publicly Held Shares;

(3) At least 300 Round Lot Holders;

(4) At least three registered and active Market Makers;

(5) In the case of ADRs, at least 400,000 issued.

(b) Initial Listing Standards for Primary Equity Securities:

(1) Equity Standard

(A) Stockholders' equity of at least $5 million;

(B) Market Value of Publicly Held Shares of at least $15 million; and

(C) Two year operating history.

(2) Market Value of Listed Securities Standard

(A) Market Value of Listed Securities of at least $50 million (current publicly traded Companies must meet this requirement and the price requirement for 90 consecutive trading days prior to applying for listing if qualifying to list only under the Market Value of Listed Securities Standard);

(B) Stockholders' equity of at least $4 million; and

(C) Market Value of Publicly Held Shares of at least $15 million.

(3) Net Income Standard

(A) Net income from continuing operations of $750,000 in the most recently completed fiscal year or in two of the three most recently completed fiscal years;

(B) Stockholders' equity of at least $4 million; and

(C) Market Value of Publicly Held Shares of at least $5 million.

As you can see, each of the standards for initial listing requires a minimum of $4 million in shareholder equity. MNKD does not meet any of these standards. I was mistaken in claiming that $5 million is required, as that only applies to option 1, Equity Standard. However, $4 million is required for all standards, which MNKD would need to meet. They currently do not.

|

|

|

|

Post by madog365 on Feb 14, 2017 13:00:23 GMT -5

|

|

|

|

Post by me on Feb 14, 2017 13:21:48 GMT -5

This question of whether NASDAQ will, "grant a 6 month extension," is really a matter of semantics.

On the one hand, MNKD will not receive a second 180-day grace period, simply because of negative shareholder equity.

On the other hand, MNKD (if the share price doesn't move to $1 for at least 10 consecutive trading days) may request a hearing once the delisting notice is issued. In this hearing, MNKD can present its plan of compliance, to include the RS. The plan would be to execute the RS if the "impending corporate actions" by themselves are not sufficient to increase the share price. This would likely result in the NASDAQ panel in allowing MNKD to execute its compliance plan - which must be executed and result in a compliant share price within 180 days.

So, depending upon what is meant by a "6-month extenstion," in the poll, the answer can be "Yes" or "No." If the 6-month extension refers to a second grace period to allow for compliance, then I vote "NO." If the 6-month extension refers to the NASDAQ panel allowing MNKD an extra 180 days to execute its compliance plan after receiving a delisting notice, then I vote "YES.

Now, can we all get back to constructive discussions, rather than arguing over semantics? Pretty please?!

|

|

|

|

Post by mnkdfann on Feb 14, 2017 13:33:32 GMT -5

let me make this easy.. I was invested in this company called Ivanhoe energy.. This company had no assets, no money and no future.. It received an 180 ext. I'd be shocked that MNKD doesn't. I'm not saying that MNKD will get the ext since no one knows.. but I'm 95% sure they will.. Ivanhoe received the initial delisting notice from Nasdaq on Jan 13 2015 and had until July 13 2015 to regain compliance. ivanhoeenergy.mediaroom.com/index.php?s=19278&item=137212Ivanhoe decided to file for bankruptcy prior to that date and was suspended from the Nasdaq on March 3 2015. It was delisted later that month. www.bloomberg.com/research/stocks/private/snapshot.asp?privcapId=666644ir.nasdaq.com/releasedetail.cfm?releaseid=902575So it received no 180 day extension, unless you are talking about some prior year delisting event. Perhaps you are confusing the Nasdaq with one of the other exchanges Ivanhoe traded on. |

|

|

|

Post by mnholdem on Feb 14, 2017 13:53:53 GMT -5

It really does come down to the interpretation of Nasdaq Listing Rule 5810(c)(3)(A)(ii)

(ii) Capital Market

If a Company listed on the Capital Market is not deemed in compliance before the expiration of the 180 day compliance period, it will be afforded an additional 180 day compliance period, provided that on the 180th day of the first compliance period it meets the applicable market value of publicly held shares requirement for continued listing and all other applicable standards for initial listing on the Capital Market (except the bid price requirement) based on the Company's most recent public filings and market information and notifies Nasdaq of its intent to cure this deficiency. If a Company does not indicate its intent to cure the deficiency, or if it does not appear to Nasdaq that it is possible for the Company to cure the deficiency, the Company will not be eligible for the second grace period. If the Company has publicly announced information (e.g., in an earnings release) indicating that it no longer satisfies the applicable listing criteria, it shall not be eligible for the additional compliance period under this rule.

---

In MannKind's case, as is the case with other biotech startup companies, I believe that the Equity Standard (one of the three standards) is simply not applicable.

Also, according to Nasdaq Listing Rule 5810(c)(3)(A)(i), The Company may also request a hearing to remain on The Nasdaq Global Market pursuant to the Rule 5800 Series.

As soon as I get the response from NASDAQ, I'll post it.

|

|

|

|

Post by mnkdfann on Feb 14, 2017 14:08:15 GMT -5

It really does come down to the interpretation of Nasdaq Listing Rule 5810(c)(3)(A)(ii)

(ii) Capital Market

If a Company listed on the Capital Market is not deemed in compliance before the expiration of the 180 day compliance period, it will be afforded an additional 180 day compliance period, provided that on the 180th day of the first compliance period it meets the applicable market value of publicly held shares requirement for continued listing and all other applicable standards for initial listing on the Capital Market (except the bid price requirement) based on the Company's most recent public filings and market information and notifies Nasdaq of its intent to cure this deficiency. ---

In MannKind's case, as is the case with other biotech startup companies, I believe that the Equity Standard (one of the three standards) is simply not applicable.

Be that as it may, Mannkind's own 8-K states: "If the Company does not regain compliance with the Minimum Bid Price Requirement by the end of the Compliance Period, under Nasdaq Listing Rule 5810(c)(3)(A)(ii), if on the last day of the Compliance Period the Company is in compliance with the market value requirement for continued listing, as well as ALL other standards for initial listing of its common stock on the Nasdaq Capital Market (other than the bid price requirement), the Company may apply to transfer the listing of its common stock to the Nasdaq Capital Market if the Company also provides written notice to Nasdaq of its intention to cure the deficiency during a second compliance period (by effecting a reverse stock split if necessary), at which point Nasdaq may grant the Company additional time to regain compliance with the Minimum Bid Price Requirement." Note the absolute unqualified use of ALL. Though I understand it is reasonable to assume Mannknd is mistaken or has no clue (based on its corporate track record to date).  |

|

|

|

Post by agedhippie on Feb 14, 2017 14:30:46 GMT -5

What I really appreciate about Mannkind is that I am exposed to all the minutiae that go on below the surface and that I don't usually get to see.  |

|