|

|

Post by nylefty on Nov 22, 2022 19:27:01 GMT -5

Some people on this board are mistakenly confusing the Part D insulin coverage under the Inflation Reduction Act (coverage which takes effect next year) and the Part D insulin coverage under the Senior Savings Model (which was a failure for MannKind this year).

Two different $35 a month programs.

|

|

|

|

Post by sayhey24 on Nov 22, 2022 20:17:46 GMT -5

Some people on this board are mistakenly confusing the Part D insulin coverage under the Inflation Reduction Act (coverage which takes effect next year) and the Part D insulin coverage under the Senior Savings Model (which was a failure for MannKind this year). Two different programs. Agreed because its not clear what CMS is doing nor what the insurers thought they were bidding on when they bid to provide Plan D and Advantage coverage under their plans. innovation.cms.gov/innovation-models/part-d-savings-modelAt the very top of the page it says The Inflation Reduction Act will cap cost-sharing for each insulin product covered under a Medicare prescription drug plan at $35 for a month’s supply beginning in January 2023. Also, Part D deductibles will not apply to these covered insulin products. The Part D Senior Savings Model, which first tested a similar benefit in Model-participating plans, will continue in 2023. This statement clearly says they are separate and says Model-participating plans, will continue in 2023. I also think this is what the insurance companies bid on and what they based their offerings on medicare.gov. The Inflation Reduction Act talks about "Selected Insulin Products" not "Covered Insulin Products" and says this The term 17 ‘selected insulin products’ means at least one of each 18 dosage form (such as vial, pump, or inhaler dosage 19 forms) of each different type (such as rapid-acting, 20 short-acting, intermediate-acting, long-acting, ultra 21 long-acting, and premixed) of insulin (as defined 22 below), when available, as selected by the group 23 health plan or health insurance issuer Thoughts? What does Selected Insulin Product mean in regards to "covered insulin products"? We can see "covered drugs" on Medicare.gov and we can see afrezza is not one of them. However in the definition on "selected insulin products" afrezza is required by law. |

|

|

|

Post by peppy on Nov 22, 2022 20:23:55 GMT -5

|

|

|

|

Post by nylefty on Nov 22, 2022 20:55:00 GMT -5

Thanks, Peppy. The Senior Savings model has been a failure for MannKind because so many Part D plans have refused to cover Afrezza. Will they relent or be forced to cover under the Inflation Reduction Act?

Let's hope so.

|

|

|

|

Post by sayhey24 on Nov 22, 2022 21:02:13 GMT -5

Thanks, Peppy. The Senior Savings model has been a failure for MannKind because so many Part D plans have refused to cover Afrezza. Will they relent or be forced to cover under the Inflation Reduction Act? Let's hope so. So true, nearly all plans have refused to cover afrezza without a pre auth. Why is that? I might need to find my tin foil cap. Here is what CMS needs to provide guidance on What does Selected Insulin Product mean in regards to " covered insulin products"? We can see "covered drugs" on Medicare.gov and we can see afrezza is not one of them. However in the definition of "selected insulin products" afrezza is required by law. |

|

|

|

Post by peppy on Nov 22, 2022 21:12:06 GMT -5

Thanks, Peppy. The Senior Savings model has been a failure for MannKind because so many Part D plans have refused to cover Afrezza. Will they relent or be forced to cover under the Inflation Reduction Act? Let's hope so. So true, nearly all plans have refused to cover afrezza without a pre auth. Why is that? I might need to find my tin foil cap. Here is what CMS needs to provide guidance on What does Selected Insulin Product mean in regards to " covered insulin products"? We can see "covered drugs" on Medicare.gov and we can see afrezza is not one of them. However in the definition of "selected insulin products" afrezza is required by law. These last 6 years have been a huge learning experience for me. One of the things I have learned is about taglines. Turns out the saying, "No one is above the law." is just a tagline. To my chagrin. |

|

|

|

Post by agedhippie on Jan 26, 2023 9:50:22 GMT -5

So here we are in 2023 and we can see how the $35 Medicare cap is implemented.

As expected (by me at least) it applies only to insulin currently in the insurer's formulary. In other words nothing changes except there is a $35 cap on the monthly bill. What has not happened is insurers being compelled to cover Afrezza because it is inhaled.

|

|

|

|

Post by sr71 on Jan 26, 2023 12:13:46 GMT -5

So here we are in 2023 and we can see how the $35 Medicare cap is implemented. As expected (by me at least) it applies only to insulin currently in the insurer's formulary. In other words nothing changes except there is a $35 cap on the monthly bill. What has not happened is insurers being compelled to cover Afrezza because it is inhaled. Bingo! Now that we are nearly a month into the new year, I'd like to see credible evidence that ANY Seniors (or anyone else for that matter) are obtaining Afrezza for a monthly out-of-pocket cost of $35. Wish I was more optimistic on this issue, but I'm expecting .....crickets for at least the near term, but maybe it'll change later on. Sports, do you think any VDEX patients have only a $35 monthly copay for Afrezza? |

|

|

|

Post by sportsrancho on Jan 26, 2023 12:26:36 GMT -5

I’ll get back to you.

|

|

|

|

Post by prcgorman2 on Jan 26, 2023 12:42:23 GMT -5

So here we are in 2023 and we can see how the $35 Medicare cap is implemented. As expected (by me at least) it applies only to insulin currently in the insurer's formulary. In other words nothing changes except there is a $35 cap on the monthly bill. What has not happened is insurers being compelled to cover Afrezza because it is inhaled. I question whether there is a difference between what the clause in the Inflation Reduction Act required with regard to a $35 cap on Medicare-covered inhalable insulin and how that's been interpreted in practice.

Without going back to review, my memory is the law required that at least one product of each form of insulin must be covered by an insurer. If that is true, then it should compel insurers to add Afrezza to their formulary in order to be in compliance with the law (because Afrezza is the only inhalable insulin on the planet). |

|

|

|

Post by prcgorman2 on Jan 26, 2023 15:24:11 GMT -5

So here we are in 2023 and we can see how the $35 Medicare cap is implemented. As expected (by me at least) it applies only to insulin currently in the insurer's formulary. In other words nothing changes except there is a $35 cap on the monthly bill. What has not happened is insurers being compelled to cover Afrezza because it is inhaled. I question whether there is a difference between what the clause in the Inflation Reduction Act required with regard to a $35 cap on Medicare-covered inhalable insulin and how that's been interpreted in practice.

Without going back to review, my memory is the law required that at least one product of each form of insulin must be covered by an insurer. If that is true, then it should compel insurers to add Afrezza to their formulary in order to be in compliance with the law (because Afrezza is the only inhalable insulin on the planet). A quick search of the phrase "dosage form" in the Inflation Reduction Act text (https://www.congress.gov/bill/117th-congress/house-bill/5376/text) provided 25 matches. I found only two instances of the phrase that seemed relevant to the question I asked in my previous post and they were both in the same subparagraph.

I think the text in blue confirms what agedhippie asserted. I think it says there is a safe harbor (i.e., statutory protection from prosecution) for high deductible health plans which do not cover "selected insulin products", and then defines "selected insulin products". I used the phrase "do not cover". The Act uses the phrase "deductible", and I'm not a lawyer so maybe I'm misinterpreting the intent.

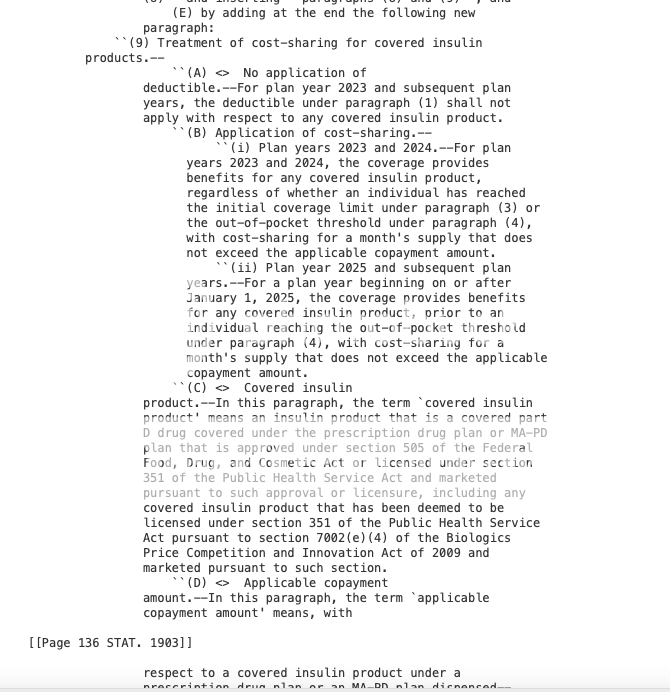

---------------------------------------------

SEC. 11408. SAFE HARBOR FOR ABSENCE OF DEDUCTIBLE FOR INSULIN.

(a) In General.--Paragraph (2) of section 223(c) of the Internal Revenue Code of 1986 <> is amended by adding at the end the following new subparagraph:

``(G) Safe harbor for absence of deductible for certain insulin products.--

``(i) In general.--A plan shall not fail to be treated as a high deductible health plan by reason of failing to have a deductible for selected insulin products.

``(ii) <> Selected insulin products.--For purposes of this subparagraph--

``(I) In general.--The term `selected insulin products' means any dosage form (such as vial, pump, or inhaler dosage forms) of any different type (such as rapid-acting, short-acting, intermediate-acting, long-acting, ultra long-acting, and premixed) of insulin.

``(II) Insulin.--The term `insulin' means insulin that is licensed under subsection (a) or (k) of section 351 of the Public Health Service Act (42 U.S.C. 262) and continues to be marketed under such section, including any insulin product that has been deemed to be licensed under section 351(a) of such Act pursuant to section 7002(e)(4) of the Biologics Price Competition and Innovation Act of 2009 (Public Law 111-148) and continues to be marketed pursuant to such licensure.''.

|

|

|

|

Post by sayhey24 on Jan 26, 2023 19:03:48 GMT -5

So here we are in 2023 and we can see how the $35 Medicare cap is implemented. As expected (by me at least) it applies only to insulin currently in the insurer's formulary. In other words nothing changes except there is a $35 cap on the monthly bill. What has not happened is insurers being compelled to cover Afrezza because it is inhaled. I question whether there is a difference between what the clause in the Inflation Reduction Act required with regard to a $35 cap on Medicare-covered inhalable insulin and how that's been interpreted in practice.

Without going back to review, my memory is the law required that at least one product of each form of insulin must be covered by an insurer. If that is true, then it should compel insurers to add Afrezza to their formulary in order to be in compliance with the law (because Afrezza is the only inhalable insulin on the planet). Just as some history the discussion on the board all started after Mike said during the Q3 call that afrezza was being covered at $35 as part of the Act. Aged then started to point out some things which did not add up. I contacted MNKD who then went to work on their side contacting CMS. I did the same with my team. In the end we both ended up with the same answer from CMS. For 2023 a pre auth would be required. Aged was right. It was not in the "covered" formularies. Once it gets approved through the pre auth process the PWD will not pay more than $35. The obvious question is why afrezza? The initial draft legislation which would have required by law to cover the inhaled form was changed. The final legislation pulled this language and pointed back to covered Medicare drugs. At the same the time MNKD had joined and was a member of the CMS Senior Saving Model but CMS did not include afrezza in the bid package. Should MNKD have kept a closer eye on the bid package, probably but it is what it is now. I think bid packages go out in March so they need to make sure afrezza is in there so it does get included into all "Plan D" coverages for 2024. At this point CMS told us both that 80% or more of the pre auths should be approved for 2023. We will just have to wait and see. There are some good social media reports of people now getting the $35 with the pre auth. Lets see what news Sports has on this. |

|

|

|

Post by sayhey24 on Jan 26, 2023 19:19:02 GMT -5

|

|

|

|

Post by agedhippie on Jan 26, 2023 20:11:43 GMT -5

... Aged then started to point out some things which did not add up. I contacted MNKD who then went to work on their side contacting CMS. I did the same with my team. In the end we both ended up with the same answer from CMS. For 2023 a pre auth would be required. Aged was right. It was not in the "covered" formularies. Once it gets approved through the pre auth process the PWD will not pay more than $35.... To be clear though. If the drug isn't in the formulary a pre-auth will not help since there is nothing to pre-authorize - the drug is not covered, period. However, where it is covered but requires a pre-authorization then it will be capped at $35 if authorized. |

|

|

|

Post by sayhey24 on Jan 26, 2023 20:38:41 GMT -5

... Aged then started to point out some things which did not add up. I contacted MNKD who then went to work on their side contacting CMS. I did the same with my team. In the end we both ended up with the same answer from CMS. For 2023 a pre auth would be required. Aged was right. It was not in the "covered" formularies. Once it gets approved through the pre auth process the PWD will not pay more than $35.... To be clear though. If the drug isn't in the formulary a pre-auth will not help since there is nothing to pre-authorize - the drug is not covered, period. However, where it is covered but requires a pre-authorization then it will be capped at $35 if authorized. I am not sure what you are saying - "the drug is not covered, period". I would say that is wrong. People on medicare whose Plan D does not "Cover" afrezza are going through a pre auth process and are getting $35 afrezza. If you look on medicare.gov it will not list afrezza as a covered drug and will show some outrageous cost. These people are in fact getting it for $35 as CMS told my team and MNKD they would. Would it be better if afrezza just showed as covered on medicare.gov, absolutely but its a small step forward. Mike and team need to be all over CMS to make sure it makes the bid packages going at in a few months for 2024 coverage. I also hope the sales reps are putting out a bulletin to all their doctors about this and explain exactly what needs to be done to get $35 afrezza. |

|