|

|

Post by parrerob on May 12, 2023 3:52:36 GMT -5

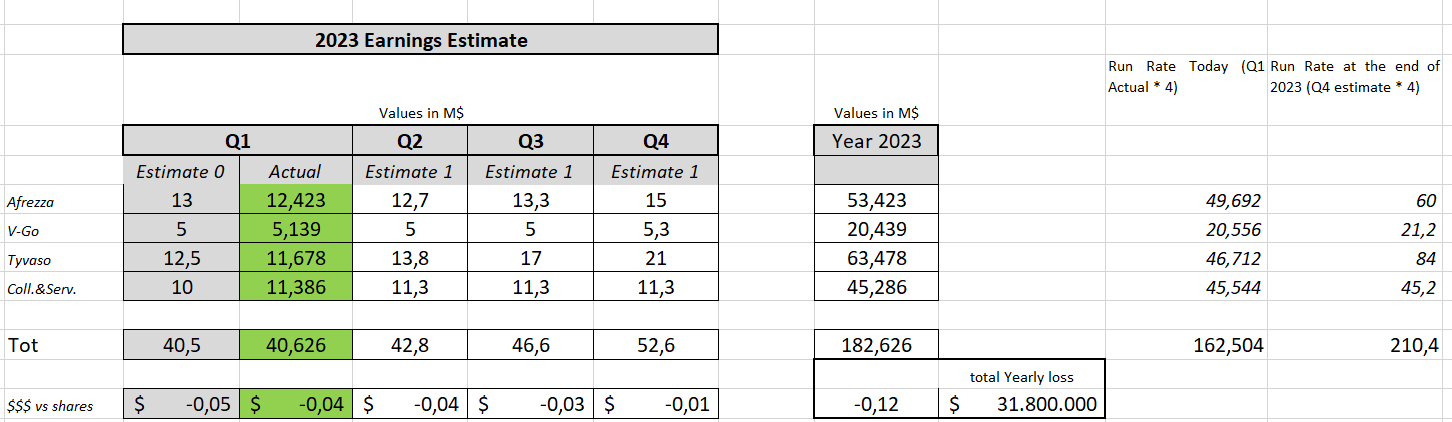

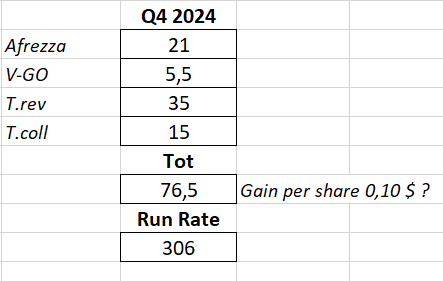

Ciao a tutti from Italy (raining today) Here is my estimate for FY23 Because of my Q1 estimate, published here 1 month ago, was quite right on revenue with a 0,2% error, I am pleased to share my Estimate for the rest of the year (adjusted now based on yesterday results).  Based on my assumption We will loose around 30 M$ in 2023 and we will see profitability just at the beginning of 2024 (but hopefully my numbers are not over estimated so We could have a nice surprise for Q4 2023 as well). We will close at 182M$ revenues with a final run rate of 200+ M$ Be advised that the loss per share calculation is based just on some interpolations I did considering total company costs Q4 2022 and Q1 2023 and the history of our past quarters (for example Q4 has been always the most expensive quarter while Q1 has been always the cheaper) PS: This is just for joke but what about Q4 2024? considering We could be near to the 10K patients on Tyvaso DPI and considering Afrezza increasing as it is doing today We could have Q4 2024 revenues at 75+M$ giving a run rate of 300+M$ (Obvioulsy considering no income from India, Brasil (re launch), Clofazimine..., Afrezza Ped etc... All of them will have impact under costs, as they are sure impacting today, but could have also some return in revenues within 2024)  PS2: Don't forget We have on a very long run, also RLS (even if no big impact this could bring some $$$ as well in the long future)…. Don't forget Qrum acquisition for pipeline development and 501 under Thirona BIO partnerhisp PS3: Don't forget We have also 300 M$ asset… the ownership of technosphere …. Many and many patents and a “huge” know how …. IMO 4B$ Market Cap evaluation TODAY (I repeat…. TODAY) should not shock anyone (15-16$ per share) IMO…. But unfortunately I am not the global market but only a little share holder (very little, very holder) |

|

|

|

Post by hellodolly on May 12, 2023 6:36:20 GMT -5

Thank you and very much appreciated.

|

|

|

|

Post by Clement on May 12, 2023 7:33:26 GMT -5

Thanks to parrerob for this clear presentation of his FY 2023 Forecast.

Parrerob's estimate for total net revenues for FY2023 is $182.6M. IMO this is very reasonable and neither fluffy nor overly optimistic.

Compare parrerob's estimate of $182.6M to the average analyst estimate of $174.9M. Only 4% difference.

Either one is a whopping increase over 2022 .

|

|

|

|

Post by alethea on May 12, 2023 8:52:07 GMT -5

Grazzi Parrerob  |

|

|

|

Post by ronw77077 on May 12, 2023 9:13:52 GMT -5

Nice job parrerob. Here's my take on the year, less quantitative than your approach, but I am a bit more optimistic.

While the stock price jumped nicely it is not reflective of the company’s value. Neither is the average analyst target price of $6.7. More on the company’s outlook below.

Key to the Q1 performance was $23 million from United Therapeutics (UT), including $12 million in royalties for producing Tyvaso-DPI (T-DPI). UT is experiencing “incredible demand” (UT’s words) for T-DPI because (a) customers are switching from the older Tyvaso Nebulizer version, and (b) T-DPI became available to clients suffering from PH-ILD (Pulmonary Hypertension with Interstitial Lung Disease). There are no other treatment options for PH-ILD. There are an estimated 30,000 patients in the U.S. with this disease. Only 10% of them are now being treated.

MNKD is increasing its T-DPI production capacity this quarter. Further, it expects to increase production by over 200% in the second half of this year. Every 10,000 patients will result in $200 million - $240 million in annual revenue to MNKD. In 2024 it will build out an additional high-volume capacity expansion. MNKD will have the capacity to treat 25,000 T-DPI patients.

Afrezza is having record sales, up 26% over Q1 in 2022.

MNKD has Pediatric trials underway to treat 4-17 years old with Afrezza. Trials should be completed in mid 2024. Every 10% share of that market will generate $150 million in annual revenues.

MNKD is also producing Clofazimine to treat nontuberculous mycobacterial lung disease. It will complete its second and final study in the second half of this year. While this is a global market, the US market is about 100,000. Every 1,000 patients on Clofazimine will generate $100 million in annual revenues to MNKD.

1,2,3

MNKD had $100 million in revenue in 2022

MNKD in on track to have over $200 million in revenue in 2023

I believe MNKD will have over $300 million in revenue in 2024, perhaps substantially more.

|

|

|

|

Post by akemp3000 on May 12, 2023 9:16:28 GMT -5

Parrerob has certainly established his status here and it's greatly appreciated. Now let's hope Mannkind can bring forth a couple of surprise additions to add to these predictions.

|

|

|

|

Post by radgray68 on May 12, 2023 11:11:55 GMT -5

Had to log in this morning just to give a thumbs up for parrerob. Thanks for that.

The global market analysts out there don't seem to have done a proper DCF model to look at all the future revenue coming our way.

|

|

|

|

Post by carefulinvestor on May 12, 2023 12:13:00 GMT -5

Also many thanks to Parrerob, great and detailed analysis - - very reasonable, not overly optimistic or pessimistic. IMY most financial so-called "analysts" could learn a lot from him/her.

|

|

|

|

Post by myocat on May 13, 2023 7:29:21 GMT -5

The breakeven could be 2nd qtr 2024.

|

|

|

|

Post by ptass on May 13, 2023 9:41:59 GMT -5

The breakeven could be 2nd qtr 2024. Probably not until the 3rd or 4th quarter as I believe the DPI rate capacity is maxed out for most of the second qtr. During the call Mike said the current limiting factor (bulk spray drying) will be improved starting in June and expects production capacity to increase by 200% in the 2nd half. |

|

|

|

Post by Clement on May 13, 2023 10:00:45 GMT -5

The breakeven could be 2nd qtr 2024. Probably not until the 3rd or 4th quarter as I believe the DPI rate capacity is maxed out for most of the second qtr. During the call Mike said the current limiting factor (bulk spray drying) will be improved starting in June and expects production capacity to increase by 200% in the 2nd half. It appears that ptass is talking about 2023. And his comments seem to support the idea that breakeven could come before Q2 2024. |

|

|

|

Post by ptass on May 13, 2023 11:01:49 GMT -5

Right you are. I read it too fast.

|

|

|

|

Post by neil36 on May 14, 2023 13:17:11 GMT -5

According to the Yahoo analysis page, the analysts estimate MNKD to lose fourteen cents this year. My guess is that almost all of that will be in the first three quarters.

The anaysts average estimate for 2024 just increased another penny to a sixteen cents a share profit (roughly $42 million)

|

|

|

|

Post by Clement on May 30, 2023 8:22:36 GMT -5

Thanks to parrerob for this clear presentation of his FY 2023 Forecast. Parrerob's estimate for total net revenues for FY2023 is $182.6M. IMO this is very reasonable and neither fluffy nor overly optimistic. Compare parrerob's estimate of $182.6M to the average analyst estimate of $174.9M. Only 4% difference. Either one is a whopping increase over 2022 . Guess what! Now, the average analyst estimate for FY2023 is $181.6M. finance.yahoo.com/quote/MNKD/analysis?p=MNKD |

|

|

|

Post by Clement on Jul 12, 2023 10:34:25 GMT -5

Thanks to parrerob for this clear presentation of his FY 2023 Forecast. Parrerob's estimate for total net revenues for FY2023 is $182.6M. IMO this is very reasonable and neither fluffy nor overly optimistic. Compare parrerob's estimate of $182.6M to the average analyst estimate of $174.9M. Only 4% difference. Either one is a whopping increase over 2022 . Guess what! Now, the average analyst estimate for FY2023 is $181.6M. finance.yahoo.com/quote/MNKD/analysis?p=MNKDNow $181.9M finance.yahoo.com/quote/MNKD/analysis?p=MNKD |

|