|

|

Post by veritasfiliatemporis on Aug 2, 2023 6:03:20 GMT -5

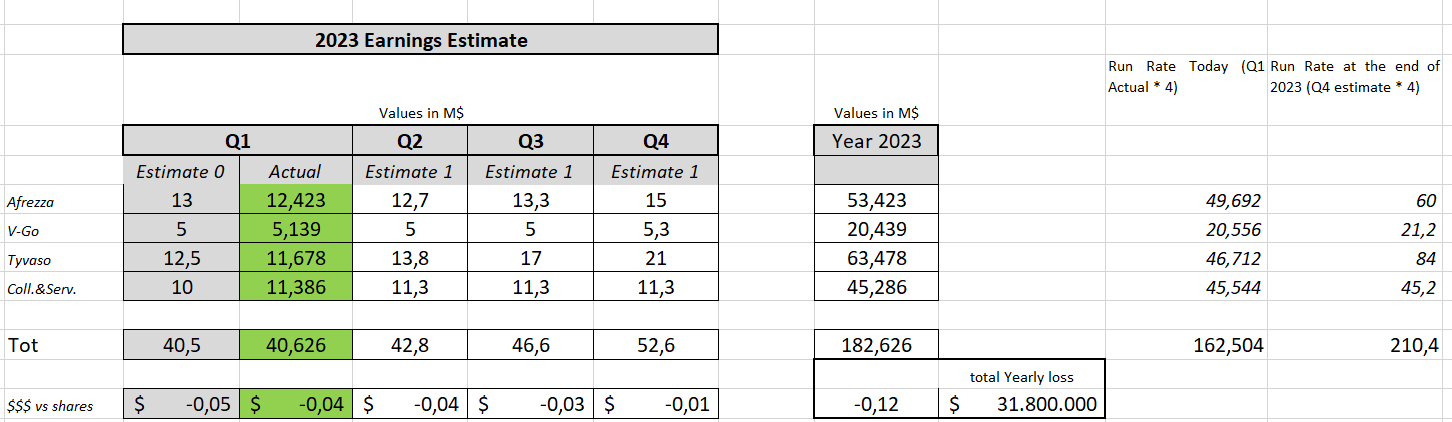

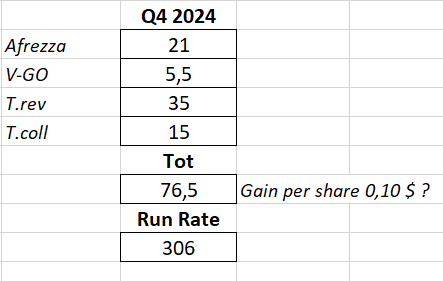

Ciao a tutti from Italy (raining today) Here is my estimate for FY23 Because of my Q1 estimate, published here 1 month ago, was quite right on revenue with a 0,2% error, I am pleased to share my Estimate for the rest of the year (adjusted now based on yesterday results).  Based on my assumption We will loose around 30 M$ in 2023 and we will see profitability just at the beginning of 2024 (but hopefully my numbers are not over estimated so We could have a nice surprise for Q4 2023 as well). We will close at 182M$ revenues with a final run rate of 200+ M$ Be advised that the loss per share calculation is based just on some interpolations I did considering total company costs Q4 2022 and Q1 2023 and the history of our past quarters (for example Q4 has been always the most expensive quarter while Q1 has been always the cheaper) PS: This is just for joke but what about Q4 2024? considering We could be near to the 10K patients on Tyvaso DPI and considering Afrezza increasing as it is doing today We could have Q4 2024 revenues at 75+M$ giving a run rate of 300+M$ (Obvioulsy considering no income from India, Brasil (re launch), Clofazimine..., Afrezza Ped etc... All of them will have impact under costs, as they are sure impacting today, but could have also some return in revenues within 2024)  PS2: Don't forget We have on a very long run, also RLS (even if no big impact this could bring some $$$ as well in the long future)…. Don't forget Qrum acquisition for pipeline development and 501 under Thirona BIO partnerhisp PS3: Don't forget We have also 300 M$ asset… the ownership of technosphere …. Many and many patents and a “huge” know how …. IMO 4B$ Market Cap evaluation TODAY (I repeat…. TODAY) should not shock anyone (15-16$ per share) IMO…. But unfortunately I am not the global market but only a little share holder (very little, very holder) I think you have to review your estimate. United Therapeutics Corporation Reports Second Quarter 2023 Financial Results......"From Net product sales from our treprostinil-based products (Tyvaso, Remodulin, and Orenitram) grew by $129.2 million, or 31%, for the second quarter of 2023, as compared to the second quarter of 2022. The growth in Tyvaso revenues resulted primarily from an increase in quantities sold to our domestic distributors of $112.0 million. $96.9 million of this growth resulted from an increased number of patients following the commercial launch of Tyvaso DPI in June 2022 and continued growth in the number of patients following the Tyvaso label expansion in March 2021 to include the treatment of pulmonary hypertension associated with interstitial lung disease." |

|

|

|

Post by parrerob on Aug 2, 2023 7:59:57 GMT -5

Yes, hopefully You are right

I will not revise my estimate, of course, but I will be very very happy to find out they were underestimated

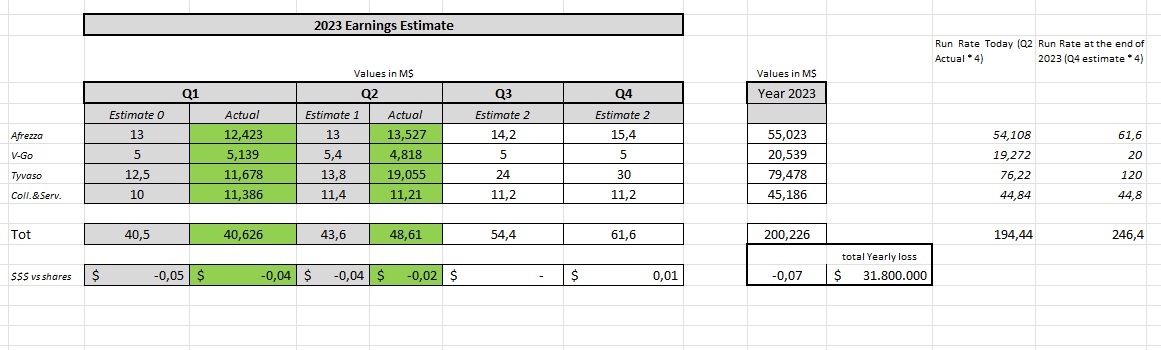

Speaking about Tyvaso We have from Q2 Earnings a total of 318,9 M$ rev

Considering Q1 related revenues were 238,4 M$ (Total Tyvaso) and MNKD revenues were 11,678 M$. So that, considering minimum 10%, We can assign to the DPI version of Tyvaso in Q1 around 116.78 M$ revenues from sales during Q1.

Also note that ratio between DPI and old Tyvaso version was probably around 49% in Q1. Assuming the same ratio in Q2 We should receive around 15,2 M$ in revenus from Tyvaso DPI (While in my Estimate1 it was 13,8 M$). So Yes We can have 1,4 M$ more giving a total rev for MNKD Q2 around 44,2 M$ (To confirm also revenues from Afrezza and V-GO)

Let's see

Regards

R.

|

|

|

|

Post by cjc04 on Aug 2, 2023 8:23:21 GMT -5

Yes, hopefully You are right I will not revise my estimate, of course, but I will be very very happy to find out they were underestimated Speaking about Tyvaso We have from Q2 Earnings a total of 318,9 M$ rev Considering Q1 related revenues were 238,4 M$ (Total Tyvaso) and MNKD revenues were 11,678 M$. So that, considering minimum 10%, We can assign to the DPI version of Tyvaso in Q1 around 116.78 M$ revenues from sales during Q1. Also note that ratio between DPI and old Tyvaso version was probably around 49% in Q1. Assuming the same ratio in Q2 We should receive around 15,2 M$ in revenus from Tyvaso DPI (While in my Estimate1 it was 13,8 M$). So Yes We can have 1,4 M$ more giving a total rev for MNKD Q2 around 44,2 M$ (To confirm also revenues from Afrezza and V-GO) Let's see Regards R. can I ask what your thoughts are on UTHR’s cost of sales going up to $36m for Q2? If MNKD received roughly $23m in revs out of UTHR’s $26m in cost for Q1, why wouldn’t we carry that comparison forward for UTHR’s Q2 cost of $36m, maybe putting us closer to $30m-$33m in total revs from UTHR? Thx |

|

|

|

Post by veritasfiliatemporis on Aug 2, 2023 8:50:51 GMT -5

I think that 49% ratio between DPI and old Tyvaso is quite conservative. "increase in quantities sold to our domestic distributors of $112.0 million. $96.9 million of this growth resulted from an increased number of patients following the commercial launch of Tyvaso DPI in June 2022" that's quite a lot compared to 318,9 total earnings. one third 96.9 of total is coming from DPI as increase from 1st to 2nd quarter, if the ratio was 50% first quarter, new ratio should be around 70% DPI 30% old Tyvaso (roughly).

|

|

|

|

Post by anderson on Aug 2, 2023 8:53:15 GMT -5

UTHR 10q 2nd quarter 11. Segment Information

Cost of tyvaso sales 40.4

13.5 mil more than last quarter.

|

|

|

|

Post by veritasfiliatemporis on Aug 2, 2023 9:21:24 GMT -5

Increase in quantities (112M$) correspond to roughly 30% increase (31% from 10Q) cost of Tyvaso sales from 27M$ to 40.4M$ roughly 34% increase , I think 45/46M$ -00.2 it is my estimate for Q2.

|

|

|

|

Post by jkendra on Aug 2, 2023 9:29:33 GMT -5

UTHR 10q 2nd quarter 11. Segment Information Cost of tyvaso sales 40.4 13.5 mil more than last quarter. Q1 2023 Tyvaso DPI Cost of Sales - 26.9M Q1 MNKD Royalty and Collab. - 23.064M Q2 2023 Tyvaso DPI Cost of Sales - 40.4M Q2 MNKD Royalty and Collab. - ? |

|

|

|

Post by tarheelblue004 on Aug 2, 2023 9:36:52 GMT -5

Exactly jkendra. If the proportion between UT cost of sales and MNKD Tyvaso revenue remains constant from Q1 to Q2, we are looking at $34.5M in Tyvaso revenue or $11.5M more than Q1.

|

|

|

|

Post by veritasfiliatemporis on Aug 2, 2023 10:13:12 GMT -5

Exactly jkendra. If the proportion between UT cost of sales and MNKD Tyvaso revenue remains constant from Q1 to Q2, we are looking at $34.5M in Tyvaso revenue or $11.5M more than Q1. I agree I only try to be conservative... |

|

|

|

Post by Clement on Aug 2, 2023 10:30:37 GMT -5

UTHR 10q 2nd quarter 11. Segment Information Cost of tyvaso sales 40.4 13.5 mil more than last quarter. Q1 2023 Tyvaso DPI Cost of Sales - 26.9M Q1 MNKD Royalty and Collab. - 23.064M Q2 2023 Tyvaso DPI Cost of Sales - 40.4M Q2 MNKD Royalty and Collab. - ? That should be "total Tyvaso" instead of "Tyvaso DPI" , right? |

|

|

|

Post by jkendra on Aug 2, 2023 10:36:31 GMT -5

Q1 2023 Tyvaso DPI Cost of Sales - 26.9M Q1 MNKD Royalty and Collab. - 23.064M Q2 2023 Tyvaso DPI Cost of Sales - 40.4M Q2 MNKD Royalty and Collab. - ? That should be "total Tyvaso" instead of "Tyvaso DPI" , right? Correct. (1) Total revenues and cost of sales include both the drug product and the respective inhalation devices for both Tyvaso and Tyvaso DPI. |

|

|

|

Post by prcgorman2 on Aug 8, 2023 15:38:28 GMT -5

Ciao a tutti from Italy (raining today) Here is my estimate for FY23 Because of my Q1 estimate, published here 1 month ago, was quite right on revenue with a 0,2% error, I am pleased to share my Estimate for the rest of the year (adjusted now based on yesterday results). Based on my assumption We will loose around 30 M$ in 2023 and we will see profitability just at the beginning of 2024 (but hopefully my numbers are not over estimated so We could have a nice surprise for Q4 2023 as well). We will close at 182M$ revenues with a final run rate of 200+ M$ Be advised that the loss per share calculation is based just on some interpolations I did considering total company costs Q4 2022 and Q1 2023 and the history of our past quarters (for example Q4 has been always the most expensive quarter while Q1 has been always the cheaper) PS: This is just for joke but what about Q4 2024? considering We could be near to the 10K patients on Tyvaso DPI and considering Afrezza increasing as it is doing today We could have Q4 2024 revenues at 75+M$ giving a run rate of 300+M$ (Obvioulsy considering no income from India, Brasil (re launch), Clofazimine..., Afrezza Ped etc... All of them will have impact under costs, as they are sure impacting today, but could have also some return in revenues within 2024) PS2: Don't forget We have on a very long run, also RLS (even if no big impact this could bring some $$$ as well in the long future)…. Don't forget Qrum acquisition for pipeline development and 501 under Thirona BIO partnerhisp PS3: Don't forget We have also 300 M$ asset… the ownership of technosphere …. Many and many patents and a “huge” know how …. IMO 4B$ Market Cap evaluation TODAY (I repeat…. TODAY) should not shock anyone (15-16$ per share) IMO…. But unfortunately I am not the global market but only a little share holder (very little, very holder) Can't wait to see the revised version. You nailed V-Go, and "Collaboration & Services" with UTHR. Afrezza was better than expected and of course the big surprise was Tyvaso at $19M versus $13.8. Still you've done a good job and I like what you've put together. |

|

|

|

Post by parrerob on Aug 21, 2023 5:39:07 GMT -5

Hello guys Here is just a quick review..... Honestly Tyvaso revenue was the key and will be the key to estimate our earnings.... Just few notes..... Afrezza total Symphony income was quite flat against Q1 so: Do we have an increase of not reported scripts ? Are we improving our ratio Gross Sales / Net Rev ? .... Any how it is still a good direction V-GO soffer... And I believe Afrezza itself is now sustainabile alone while the fact that the area will be sustainable in 2024 it is beacuse of V-Go losses (sales are flat and no changes till the time We bought V-GO..... V-GO brings 20 M$ net rev but probably it costs a lot more to sell it...) Coll&Services: back to flat as declared during Q4-22 call Tyvaso DPI: How can We estimate it ? We know the history and some few facts like the increased production from middle Q2, like 10K patients at the end of 2024 = around 220M$ net revenues ? How will be the path ? Personally I considered another 5M$ increase for Q3 then another 6M$ increase for Q4 but it is like a lottery for me.... Feel free to add Your comments but please be conservative..... Much better to have a positive surprise then a negative one !!! |

|

|

|

Post by ktim on Aug 21, 2023 14:59:15 GMT -5

Yet another analyst upgrade  |

|

|

|

Post by cedafuntennis on Aug 21, 2023 17:36:58 GMT -5

Yet another analyst upgrade What analyst? Could u please provide a link or a copy? |

|