|

|

Post by runner on Aug 22, 2023 20:59:03 GMT -5

Good word! I'm gonna use it...thanks.

|

|

|

|

Post by parrerob on Nov 9, 2023 7:49:02 GMT -5

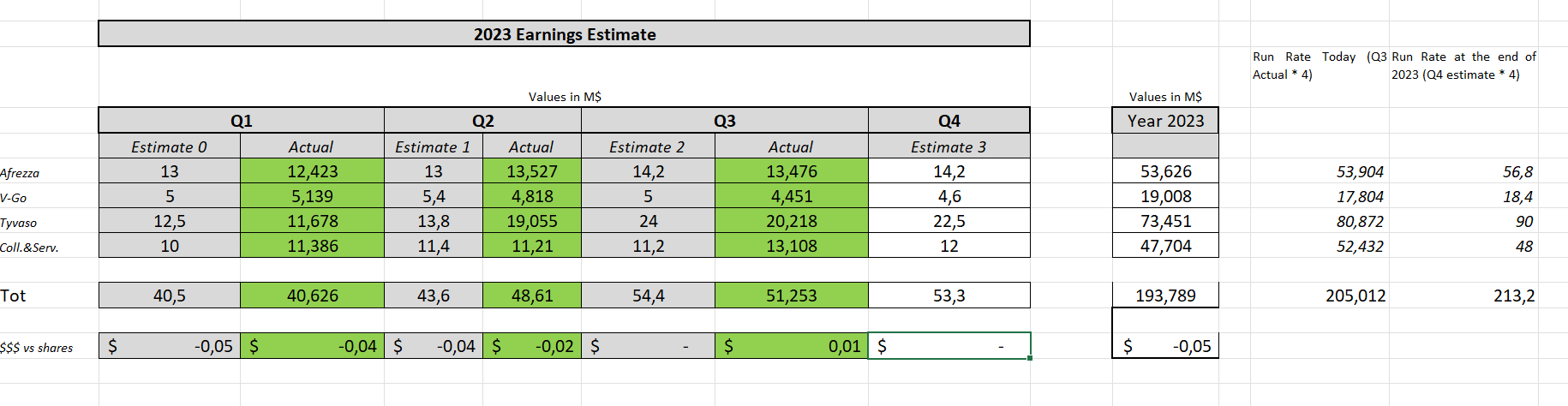

Here we are, friends of Proboard After Tuesday's call I updated the revenue scheme for 2023.  Honestly, I still need some time to assimilate Q3 data... Apart the revenues from Tyvaso DPI which are very difficult to evaluate and estimate for the future, I have many doubts about the collaborations & services part: we had a notable increase from Q1 to Q2 on the revenues side ( +60%) and collaborations & services remained flat (indeed slightly decreased) while we now have a notable increase (close to 20%) from Q2 to Q3 when revenues instead had a much more limited increase (+6%)… Possible that this value has a relationship with the previous quarter (don’t think so… but) ? Also amazed by the revenues from Afrezza… despite an increase from Symphony, revenues decreased slightly compared to Q2. OK it can be. Best Regards to all Rob. |

|

|

|

Post by Clement on Nov 9, 2023 8:46:23 GMT -5

Here we are, friends of Proboard After Tuesday's call I updated the revenue scheme for 2023. Honestly, I still need some time to assimilate Q3 data... Apart the revenues from Tyvaso DPI which are very difficult to evaluate and estimate for the future, I have many doubts about the collaborations & services part: we had a notable increase from Q1 to Q2 on the revenues side ( +60%) and collaborations & services remained flat (indeed slightly decreased) while we now have a notable increase (close to 20%) from Q2 to Q3 when revenues instead had a much more limited increase (+6%)… Possible that this value has a relationship with the previous quarter (don’t think so… but) ? Also amazed by the revenues from Afrezza… despite an increase from Symphony, revenues decreased slightly compared to Q2. OK it can be. Best Regards to all Thanks, parrerob! Very nice analysis! Could I interest you in a slight increase in T-DPI revs for Q4? In a recent post by standup, there's a good argument for adding $4M to Q3. See the post at mnkd.proboards.com/post/257748/thread(The addition of $4M per quarter also corresponds to addition of 500 T-DPI patients per quarter.) |

|

|

|

Post by parrerob on Nov 9, 2023 11:27:51 GMT -5

I know Clement.... but I ve read a lot of opinion about it and also I based my assumption on the fact that I remember that Tyvaso DPI was expecting good sales in Q2 and Q3 ....

And I can confess that I continue to update the table mainly to have quickly an idea on the full year... the run rate... and start having history on revenues streams (without having every time to open MannKind web page)... So I am not putting a strong effort in the estimate but just on trying to analyze the history (from the next one I will take out historic estimate from the table).

Also I prefer to be conservative ...

Thanks

|

|

|

|

Post by parrerob on Jan 22, 2024 4:38:01 GMT -5

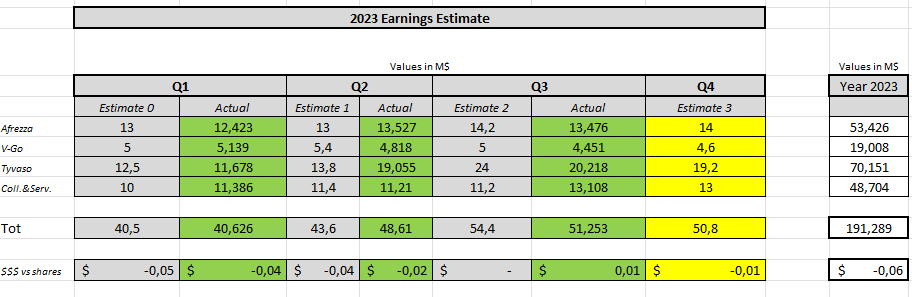

Dear all just time to think about Q4 2023 Earning Call... I did a review following the recent news (mainly the 9% instead of 10% related to Tyvaso DPI stream)  Supposed an increase of 5% on Tyvaso DPI sales (Q4 vs Q3)… then 9% on UTHR revenues (instead of previous 10%) Supposed a -0,01 on EPS as statistically q4 is the most expensive quarter (also Mike gave us an anticipation of this). Then Just to have an idea I started the 2024 estimate table....... ASSUMPTIONS - For Afrezza just small increments (hopefully) - Collaborations and Services fixed around 13 million $ per quarter. - Vgo as I feel it, just on small downtrend - No other net rev streams in 2024 (hopefully We will add something for 2025) - No India / CIPLA streaming on this estimate…. (because of no info and anyhow small expectations from India) Change numbers as You prefer but more or less untill new streams arrive We are really stack around 0 EPS for the whole 2024.  |

|

|

|

Post by parrerob on Jan 22, 2024 4:55:22 GMT -5

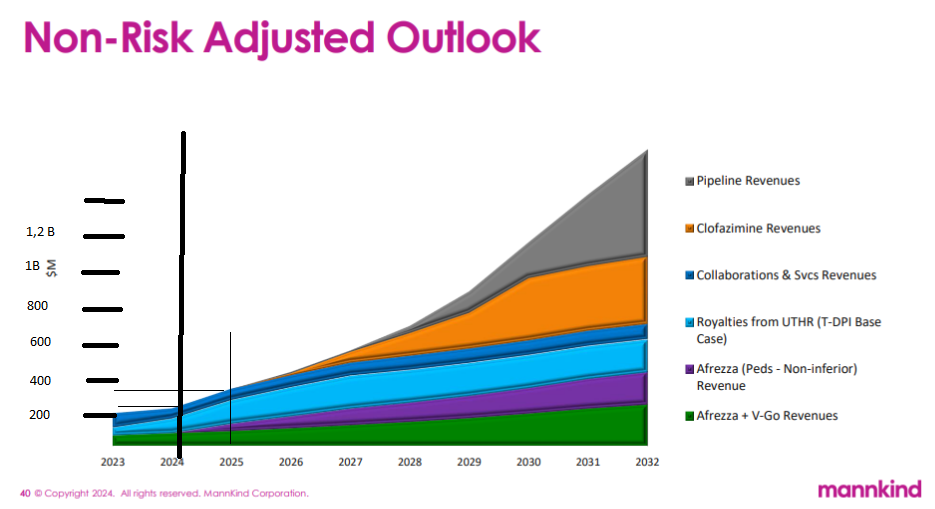

This is the long term revenue forecast presented by MNKD during last MS event. 2024 seems just in line with 2023 (let me say 220 M$ / year) then starting from 2025 the revenue stream start increasing towards around 350 M$ / year. In the next 10 years, following this forecast, We should have around 1,6 / 1,8 B$ revenue... WOW I will be very happy if the 450/500 Million $ expected for 2026 will be true... that's only a couple of years ! |

|

|

|

Post by cretin11 on Jan 22, 2024 6:51:05 GMT -5

Thanks parrerob for the well thought out estimate.

|

|

|

|

Post by castlerockchris on Jan 22, 2024 13:14:00 GMT -5

This is the long term revenue forecast presented by MNKD during last MS event. 2024 seems just in line with 2023 (let me say 220 M$ / year) then starting from 2025 the revenue stream start increasing towards around 350 M$ / year. In the next 10 years, following this forecast, We should have around 1,6 / 1,8 B$ revenue... WOW I will be very happy if the 450/500 Million $ expected for 2026 will be true... that's only a couple of years ! I believe I heard MC say during the presentation that the chart was for illustrative purposes only and designed to show the potential of the lines. When I heard this I took it to mean that the numbers on the chart were not a forecast or prediction, but simply designed to show the potential MNKD revenue streams in out years. I would not read much in the actual numbers in the intersection points. |

|

|

|

Post by Clement on Jan 22, 2024 14:00:42 GMT -5

I'm not an accountant but I think that when MNKD reports revenues, they will report the full 10% royalties revenue received from UTHR. As a separate accounting issue, the amount due Sagard will be handled. This affects profitability but no adjustment is needed for revenue estimates.

|

|

|

|

Post by thekid2499 on Jan 22, 2024 14:10:30 GMT -5

If we were doing $450 to $500 million in 2026, what is reasonable expectation for our stock price if it was fairly valued? Anyone have thoughts on this?

|

|

|

|

Post by prcgorman2 on Jan 22, 2024 15:58:57 GMT -5

If we were doing $450 to $500 million in 2026, what is reasonable expectation for our stock price if it was fairly valued? Anyone have thoughts on this? I'm a fan of fundamentals. I was taught price per share can be estimated by Earnings Per Share (EPS) multiplied by Price to Earnings (P/E) ratio. Note that the average P/E ratio can be found for a market (e.g., NASDAQ) or sector (e.g., Pharma - Drugs). Note also that sales revenue is not the same as earnings.

The current market cap on MNKD is $924,642,000 (per Yahoo!). If we divide the market cap by price per share, shares outstanding is approximately 269,574,927.

$450,000,000 in revenue - 51% in expenses yields earnings of $220.5M divided by 269,574,927 is ~$0.82 EPS.

$500,000,000 in revenue - 51% in expenses yields earnings of $245M divided by 269,574,927 is ~$0.91 EPS.

The average P/E for NASDAQ is ~25.71 and the average P/E for Pharma-Drugs is 38.94 (per NYU).

Therefore, the estimated Price Per Share for $220,500,000 in earnings is $0.82 x 25.71 = $21.03 (NASDAQ average P/E) or $0.82 x 38.94 = $31.85 (NYU Pharma-Drugs average P/E).

The estimated Price Per Share for $500,000,000 in earnings is $0.91 x 25.71 = $23.37 (NASDAQ average P/E) or $0.91 x 38.94 = $35.39 (NYU Pharma-Drugs average P/E).

A recent short discussion on P/E argued that a ratio of 17:1 was more appropriate. This is MNKD, so perhaps a more conservative estimate like 17:1 P/E is more realistic. Also, the 51% expense ratio was taken from a chart of large pharma company expense ratios and may not be appropriate for MNKD. Actual net income is available in the income statements and can be used to create a more accurate estimate, but I was too lazy to look up income statements and create an estimate. Caveat emptor.

The bottom-line is using a generous expense and a couple of average P/E ratios, $450M to $500M in revenue should yield price per share between ~$21 and ~$35.

|

|

|

|

Post by parrerob on Jan 22, 2024 16:05:37 GMT -5

This is the long term revenue forecast presented by MNKD during last MS event. 2024 seems just in line with 2023 (let me say 220 M$ / year) then starting from 2025 the revenue stream start increasing towards around 350 M$ / year. In the next 10 years, following this forecast, We should have around 1,6 / 1,8 B$ revenue... WOW I will be very happy if the 450/500 Million $ expected for 2026 will be true... that's only a couple of years ! I believe I heard MC say during the presentation that the chart was for illustrative purposes only and designed to show the potential of the lines. When I heard this I took it to mean that the numbers on the chart were not a forecast or prediction, but simply designed to show the potential MNKD revenue streams in out years. I would not read much in the actual numbers in the intersection points. You are totally right CastleR. But it Was presented by a CEO in front of MS event… not during a pizza with friends…. If the board is not able to reach the potential that is another story There are also dates that match with what we know…. So at least this table is a naïf forecast of revenue stream done by our CEO and sure is better then mine or others Note the non inferior on ped |

|

|

|

Post by sayhey24 on Jan 22, 2024 16:15:33 GMT -5

Maybe if Mike can square away afrezza's 3 issues and introduces Saxenda DPI we could have a P/E like DXCM's 140.

|

|

|

|

Post by ktim on Jan 22, 2024 20:06:37 GMT -5

If we were doing $450 to $500 million in 2026, what is reasonable expectation for our stock price if it was fairly valued? Anyone have thoughts on this? I'm a fan of fundamentals. I was taught price per share can be estimated by Earnings Per Share (EPS) multiplied by Price to Earnings (P/E) ratio. Note that the average P/E ratio can be found for a market (e.g., NASDAQ) or sector (e.g., Pharma - Drugs). Note also that sales revenue is not the same as earnings.

The current market cap on MNKD is $924,642,000 (per Yahoo!). If we divide the market cap by price per share, shares outstanding is approximately 269,574,927.

$450,000,000 in revenue - 51% in expenses yields earnings of $220.5M divided by 269,574,927 is ~$0.82 EPS.

$500,000,000 in revenue - 51% in expenses yields earnings of $245M divided by 269,574,927 is ~$0.91 EPS.

The average P/E for NASDAQ is ~25.71 and the average P/E for Pharma-Drugs is 38.94 (per NYU).

Therefore, the estimated Price Per Share for $220,500,000 in earnings is $0.82 x 25.71 = $21.03 (NASDAQ average P/E) or $0.82 x 38.94 = $31.85 (NYU Pharma-Drugs average P/E).

The estimated Price Per Share for $500,000,000 in earnings is $0.91 x 25.71 = $23.37 (NASDAQ average P/E) or $0.91 x 38.94 = $35.39 (NYU Pharma-Drugs average P/E).

A recent short discussion on P/E argued that a ratio of 17:1 was more appropriate. This is MNKD, so perhaps a more conservative estimate like 17:1 P/E is more realistic. Also, the 51% expense ratio was taken from a chart of large pharma company expense ratios and may not be appropriate for MNKD. Actual net income is available in the income statements and can be used to create a more accurate estimate, but I was too lazy to look up income statements and create an estimate. Caveat emptor.

The bottom-line is using a generous expense and a couple of average P/E ratios, $450M to $500M in revenue should yield price per share between ~$21 and ~$35.

The IBB has 17.7 P/E and the IHE lists 18.9. Assuming 39 P/E for a particular time point in the future seems a bit of wishful thinking. Possible, sure, but we could also be in a period of multiple compression in pharma rather that that sort of huge expansion. Of course any given stock could have significantly better or worse P/E than the average based on the outlook for future revenue earnings growth. If Mike can execute on the revenue growth he shows, I'm 100% positive I'll be thrilled with the share price. |

|

|

|

Post by prcgorman2 on Jan 22, 2024 23:57:49 GMT -5

I should probably mention I think Mike’s chart was possibly showing net income, so the calculations really would be $450M to $500M, not the discounted amounts I was using for the price per share calculations.

|

|